Don’t Buy Realty Income, Buy STORE Capital Instead

- O is the world’s largest triple net lease REIT with a stellar track record.

- STOR also boasts significant scale and an impressive track record.

- We discuss why STOR is a better buy than O at the moment.

Realty Income (NYSE:O) is the world’s largest triple net lease REIT with a massive enterprise value of $58.1 billion. O has trademarked and assigned itself the name The Monthly Dividend Company to reflect its devotion togenerating stable and steadily growing monthly dividend checks for shareholders.

O owns over 6,500 real estate properties, virtually all of which are secured by long-term, conservatively structured, triple net leases. As a result, it has one of the most stable cash flow profiles in the market today, enabling it to pay out over 600 consecutive common stock monthly dividends over the course of 52 years, while also increasing the dividend payout by 109 times since going public in 1994.

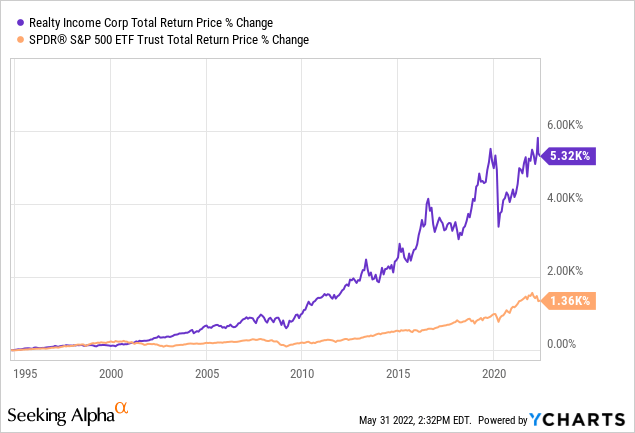

As a result, it is a Dividend Aristocrat and has generated tremendous total returns for shareholders since going, crushing the broader market (SPY) in the process:

STORE Capital (NYSE:STOR) is also a triple net lease that – while not nearly as large as O – is still large with an enterprise value of $12.2 billion and over 2,500 individual real estate properties.

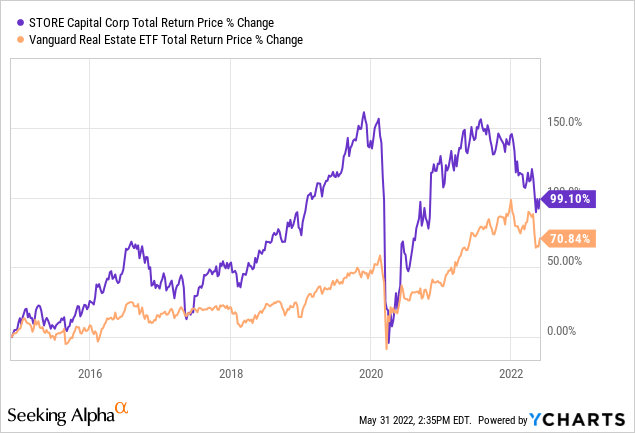

As a result, it also enjoys a very stable cash flow profile and has managed to grow its dividend every year since going public as well. On top of that, STOR has outperformed the REIT index (VNQ) since going public:

In this article, we will discuss why we are more bullish on STOR than O in the current environment and are long STOR stock instead of O.

O Stock Bull Case: Unparalleled Track Record & Safety

There is obviously a lot to like about O stock. First and foremost, the company’s world-leading scale, sector-leading credit rating, and fantastic track record give it significant competitive advantages, including access to many deals that smaller competitors cannot afford to bid on (for example, its recent multi-billion dollar acquisition of VEREIT), the resources to attract the best and brightest talent in the sector, a strong information edge which it can leverage to generate outperformance, and a cost of capital advantage thanks to its superior credit rating and the attractiveness of its equity to so many income investors.

O’s diversification is truly phenomenal, as it serves ~1,090 clients across 70 industries in all 50 U.S. states as well as in Puerto Rico, the United Kingdom, and Spain. Its top clients are very stable, highly profitable, and ecommerce and recession-resistant businesses as well. They include Walgreens (WBA), 7-Eleven, Dollar General (DG), Dollar Tree (DLTR), FedEx (FDX), LA Fitness, CVS (CVS), Walmart (WMT), Tractor Supply (TSCO), and Home Depot (HD).

When combined with its substantial liquidity and well-laddered debt maturity profile, the company deserves every bit of its A3/A- credit ratings from Moody’s and S&P, respectively.

On top of that, the stock price is fairly attractive looking here when you combine the company’s stellar track record and very conservative positioning with the 4.3% dividend yield, 18.94x EV/EBITDA ratio (compared to its five year average EV/EBITDA ratio of 20.15x), and 17.25x price to FFO ratio (compared to its five year average price to FFO ratio of 18.74x).

On top of that, the growth outlook is pretty good as well with FFO per share expected by analysts to grow at a near 7% CAGR over the next half decade and the dividend per share to grow at a 5% CAGR. With the company able to close massive deals like the acquisition of VEREIT on such accretive terms (10%+ accretive to AFFO per share immediately upon closure with $45-$55 million in annual G&A synergies expected), O should be able to sustain needle-moving growth for the foreseeable future.

STOR Stock Bull Case: Higher Yield & High Growth

While O certainly has the track record and competitive advantages that make it look like an attractive investment right now, the main reason why we like STOR more is that the company offers investors a much more attractive total return proposition without them having to take on much more risk.

Analysts expect FFO per share to grow at a similar clip at STOR as it currently is at O. While O benefits from access to larger deals and has a lower cost of capital than STOR does, STOR does not have the law of large numbers working against it quite like O does. Furthermore, it invests in middle-market, non-investment grade tenants whereas O focuses on larger, mostly investment grade tenants. While you would think that this means that O is much lower risk than STOR is, the reality is that STOR focuses on property-level economics to mitigate risk. Between its direct origination platform, customer-centric approach (approximately one-third of new business comes from existing customers), use of diversification, and selectivity within its enormous $3.9 trillion total addressable market, STOR is able to keep risks low (4.7x rent coverage of its properties) while buying new properties at superior cap rates that offset its higher cost of capital relative to O’s.

Its balance sheet is also quite strong, earning it a solid BBB credit rating from S&P. It boasts a well-laddered debt maturity schedule, with minimal debt due prior to 2024 and maturities well distributed between 2024 and 2034 so that no year presents a massive wall of maturities that need to be dealt with. Its debt service coverage ratio is also an extremely conservative 7.1x, putting it in excellent shape to meet its financial obligations.

Meanwhile, its valuation is much cheaper than O’s. It trades at a mere 14.83x on an EV/EBITDA basis (4.11 turns lower than O’s) and a 12.66x on a price to FFO basis (4.59 turns lower than O’s) while offering investors a forward dividend yield of 5.8% (150 basis points superior to O’s).

Given that the primary bear thesis facing triple net lease REITs today is high inflation, we believe that STOR’s yield plus growth rate of ~13-14% gives it a compellingly superior risk-reward to O’s, given that it offers investors a mere ~11%% yield plus growth rate with only marginally lower risk.

Investor Takeaway

The main bear case for the triple net lease REIT sector right now is that we have four-decade high inflation rates, rendering the typical triple net lease REIT’s contractually fixed rent escalations of 1-2% insufficient to sustain the purchasing power of cash flows coming from these contracts.

That said, in addition to the aforementioned reasons, we remain bullish on the likes of O and especially STOR because:

- The Federal Reserve is raising rates aggressively to fight inflation. While the expectation is that this will send the economy into recession, triple net lease REITs like STOR and O with conservative lease structures, massive diversification, and strong balance sheets tend to weather recessions quite easily.

- While rising interest rates can reduce incremental profitability by squeezing investment spreads and also lead to multiple compression on the stock price, cap rates generally follow interest rates higher over time. As a result, triple net lease REITs typically have the profit margins on incremental property acquisitions restored within a few quarters. REITs are then able to lock in these higher cap rates over multi-decade contracts while they can relatively easily refinance the debt attached to them whenever interest rates decline again. The net result is improved profitability.

As a result, we expect both O and STOR to be able to weather the current unfavorable macro environment fairly well, and therefore view the current discounted share prices as a good opportunity to buy.

The increasingly accepted notion that we are headed for an inflationary recession is prompting leading investors like Ray Dalio to urge investors to seek out “real returning” investments. With inflation appearing to peak in the high single digits, O and STOR should serve investors fairly well as conservative investments through a period of stagflation since they offer yields plus growth rates that will likely exceed 10% for the foreseeable future while also providing strong recession resistance and low downside risk for investors.

That said, we are concentrating our Core Portfolio allocation to triple net lease REITs into STOR and skipping over O due to the fact that STOR’s yield plus growth is substantially superior to O’s while the downside risk is only minimally greater for STOR. Hence, STOR’s risk-reward is significantly greater than O’s, making it a Strong Buy whereas we only view O as a Buy.