Retirement Strategy: 5 ETFs For Safely Adding A 7% Yield To Your Portfolio

If added smartly, these ETFs can be great opportunities to boost your retirement income.

The income investing landscape for retirees has improved somewhat throughout 2022. Granted, that’s come on the heels of falling stock and bond prices, but available yield opportunities in both markets today are becoming more attractive.

This is especially true on the fixed income side. For example, 10-year Treasuries, which were yielding a scant 0.5% a little over two years ago, touched the 3% level in July. Even 3-month Treasury bills, which yielded next to nothing, can be purchased today with a yield north of 2.5%. Existing shareholders have had a rough ride over the past year, but the yield/risk tradeoff today is much improved.

On the equity side, the S&P 500 and the dividend aristocrats are still only offering 1.5% to 2% yields, but ETFs that focus more on high yielders, such as the iShares Select Dividend ETF (DVY) or the Invesco S&P 500 High Dividend Low Volatility ETF (SPHD), are currently paying 3.5% to 4% annually.

Retirees and income seekers no longer need to venture far out on the risk spectrum to capture a reasonable yield.

Reaching for HIGH yields, I’m talking in the range of 7% or more, usually comes with inherently more risk regardless of the environment. These should always be approached with caution and a level of skepticism before jumping in. That’s not to say that stocks or ETFs that offer high yields are inappropriate by any stretch, but investors should be well aware of the risks and downside that come with them.

When researched properly and added to a portfolio smartly, however, they can be great yield-enhancing opportunities. Each takes a bit of a different approach to yield generation. Some use options strategies. One targets liquid alternative asset classes. None of these are highly speculative home run swings, but investors should understand what’s under the hood before taking them for a test drive.

For that reason, I’m going to discuss 5 ETFs that currently offer at least a 7% forward-looking yield that I think are worth considering for your retirement portfolio.

Let’s break them down.

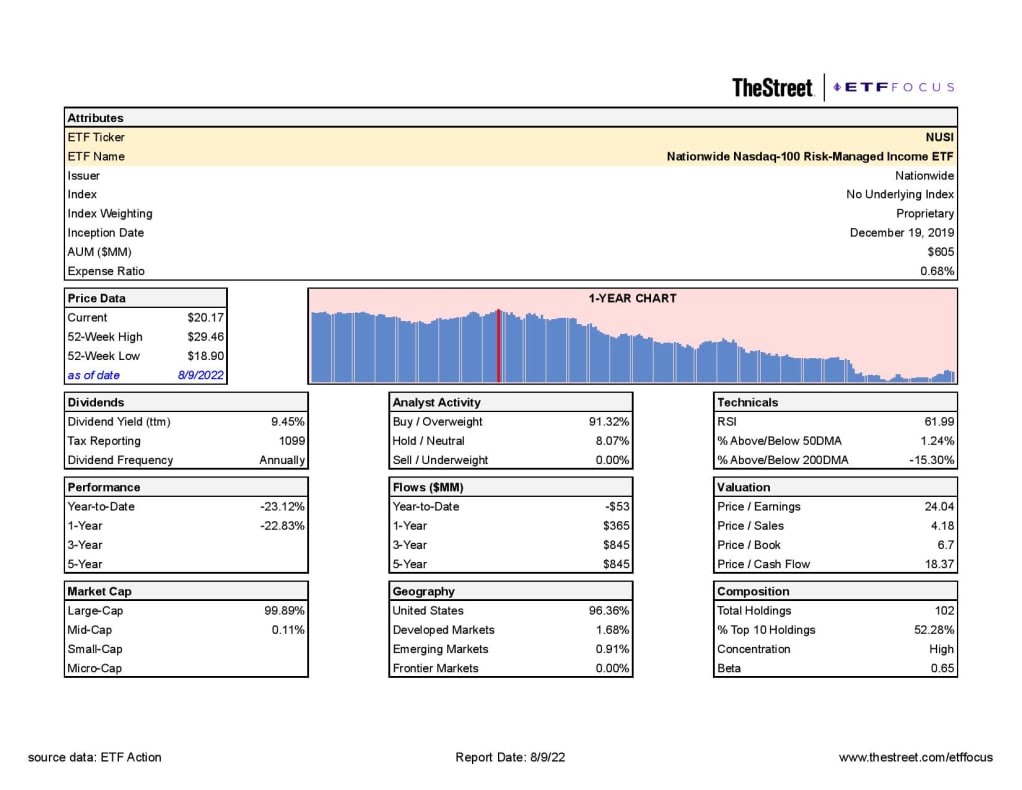

Nationwide Nasdaq 100 Risk Managed Income ETF (NUSI)

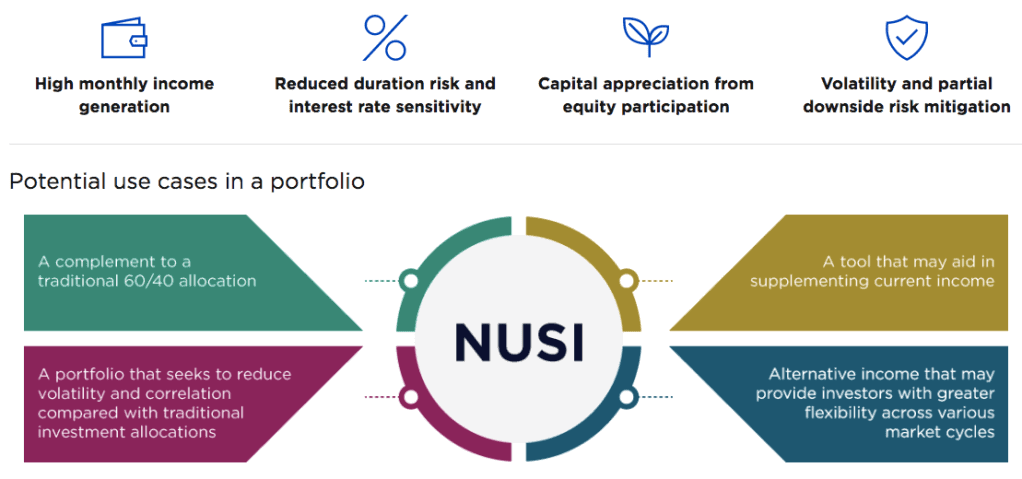

When it comes to high yield ETF choices, NUSI is a fund I bring up often. Its 7.8% yield is the biggest selling point, but the real key could be the options collar strategy that reduces volatility and downside risk, especially in the current market environment.

To start, NUSI fully replicates the Nasdaq 100 as the core position in the portfolio. From there it layers on a combination of written call options with purchased put options on the index. These options positions are intended to generate a “net credit” position, meaning that the premiums received from the written calls outweigh the premiums paid for the puts. The dividend income received from the underlying Nasdaq 100 investment is relatively small. It’s the options income that generates the big yield.

It’s important to understand that those options positions alter NUSI’s risk/return profile. The puts protect against some level of downside risk, but the written calls also put a cap on upside potential. Think of it as the options collar limiting the range of returns on both ends in exchange for the high yield.

NUSI has struggled in 2022. The core Nasdaq 100 investment has declined by about 20% and the options collar has failed to help out much. The monthly income (another advantage of NUSI) has declined in recent months, probably a function of puts becoming much more expensive and calls becoming less so. The downside risk hedge, however, has still been effective. Over the past year, NUSI has only experienced about 85% of the downside of the Nasdaq 100.

As a pure income option, however, the high yield/managed risk aspect of the fund is attractive. There are also options investing in the S&P 500 (NSPI), the Dow 30 (NDJI) and the Russell 2000 (NTKI).

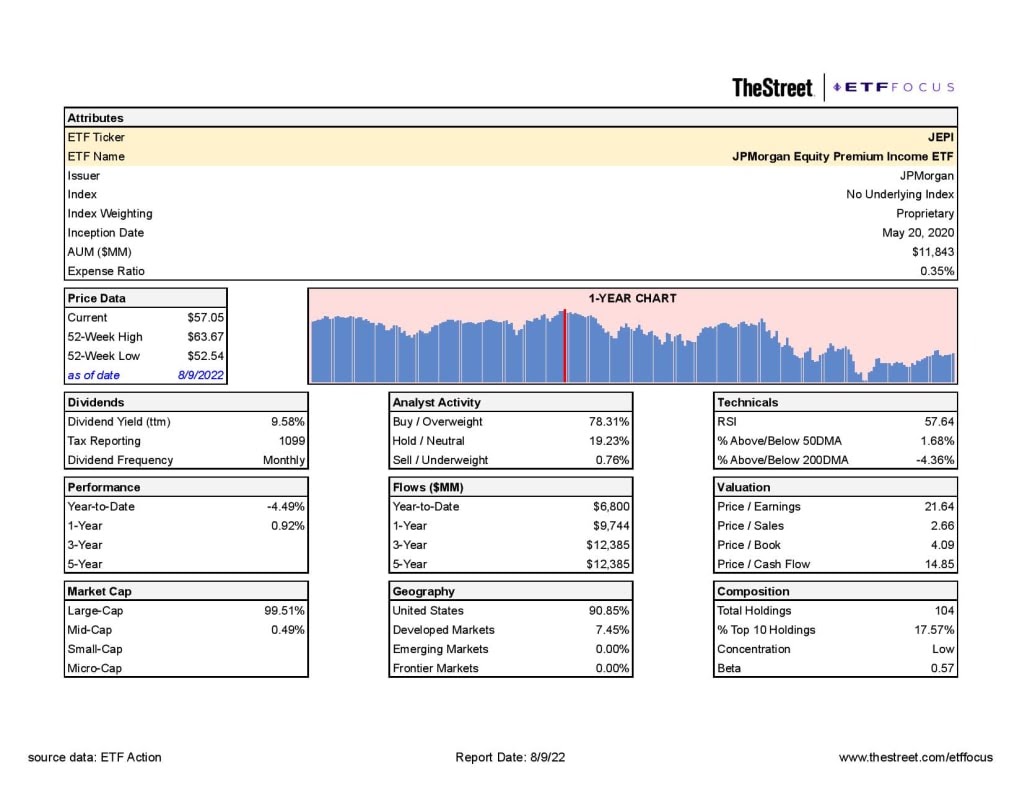

JPMorgan Equity Premium Income ETF (JEPI)

Here’s another of my favorite high income ETFs. With more than $11 billion in assets, this one has gotten a lot of attention and become a big hit with income seekers. Fundamentally, its strategy is pretty straightforward and simple (although the execution of it is a bit unique). JEPI quotes an extraordinary 12% yield right now. Historically, the fund has paid somewhere in the range of around 8% and is probably where investors should expect it over the long-term. The 12% yield is nice for now, but probably unsustainable.

JEPI is more of your traditional covered call strategy and consists of two parts. The first sleeve is a core portfolio of low volatility stocks that are mostly, if not entirely, from the S&P 500. Right now, the fund maintains about 100 holdings with volatility levels about 30% less than that of the S&P 500. Like NUSI, JEPI pays out distributions on a monthly basis.

The second sleeve involves the covered calls. To accomplish this, JEPI invests in equity-linked notes (ELNs), which are essentially a position in the S&P 500 with the written call option all rolled into a single security. It’s a little unusual to approach covered call strategies in this manner, although I think it’s a minor nitpick. Overall, JEPI invests 80% in low volatility stocks and 20% in ELNs.

JEPI is just over two years old, so there’s not a lot of history to work with, but we can see a distinct trend where the fund underperforms when stocks are doing well but outperforms when stocks are weak. Year-to-date, JEPI is beating the S&P 500 by 8%.

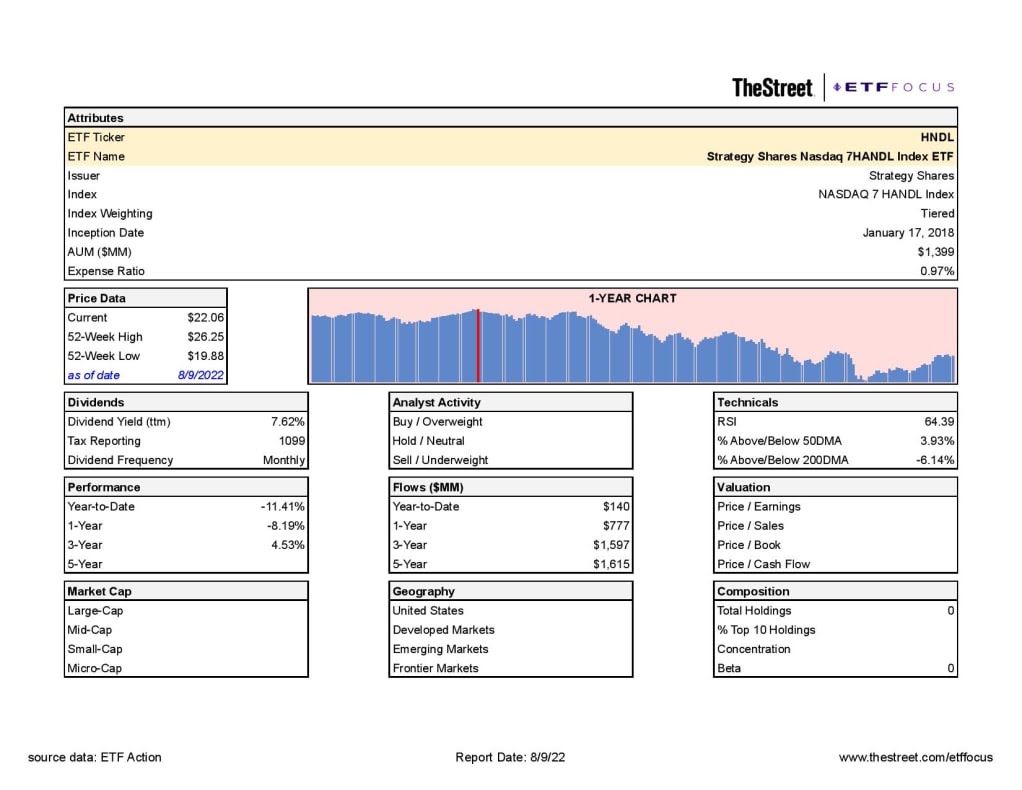

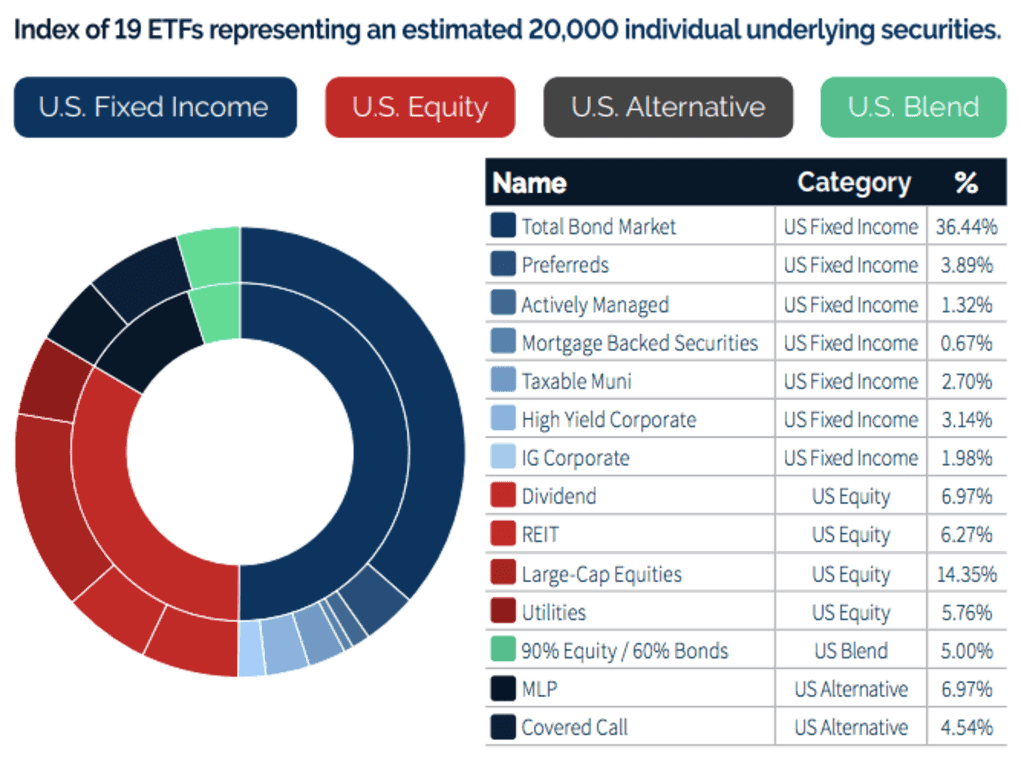

Strategy Shares Nasdaq 7HANDL Index ETF (HNDL)

HNDL is one of the most fully diverse ETFs you’ll find. It’s a fund-of-funds that holds positions in 19 different ETFs, including stocks, fixed income, preferreds, covered calls, REITs and munis among others. While it doesn’t maintain a target allocation, its current allocation is about 50% fixed income, 40% equities and 10% alternatives.

HNDL builds its portfolio by splitting it into two pieces – a “core” portfolio, which is more a standard mix of equity and fixed income ETFs, and an “explore” portfolio, which employs a tactical allocation across stocks, bonds and alternatives that traditionally offer high yields. On top of all that, HNDL uses leverage of approximately 23% of total net assets in order to enhance total return and yield potential.

The “7HANDL” part of the ETF’s name come from its distribution plan, where it pays shareholders an annualized 7% target yield split into monthly payments. In that way, the monthly distribution is tied to the fund’s share price. As HNDL’s share price rises, so too does the monthly payment. As prices decline, as they have in 2020, the distribution falls.

One thing to keep in mind with this ETF is that since its distributions can consist of returns of capital. If the fund isn’t able to generate the income or capital gains necessary to meet the 7% annualized yield target, it needs to take fund assets to make up the difference. Essentially, it’s giving you your own investment back as a distribution. Reductions in the fund’s asset base due to things like this can reduce the NAV over time if it happens consistently. Some closed-end funds run into this issue if they overdistribute, which results in steadily declining share prices. According to the fund’s latest annual report, there was a very minor return of capital distribution made. It’s not a problem at this point, but something to be aware of.

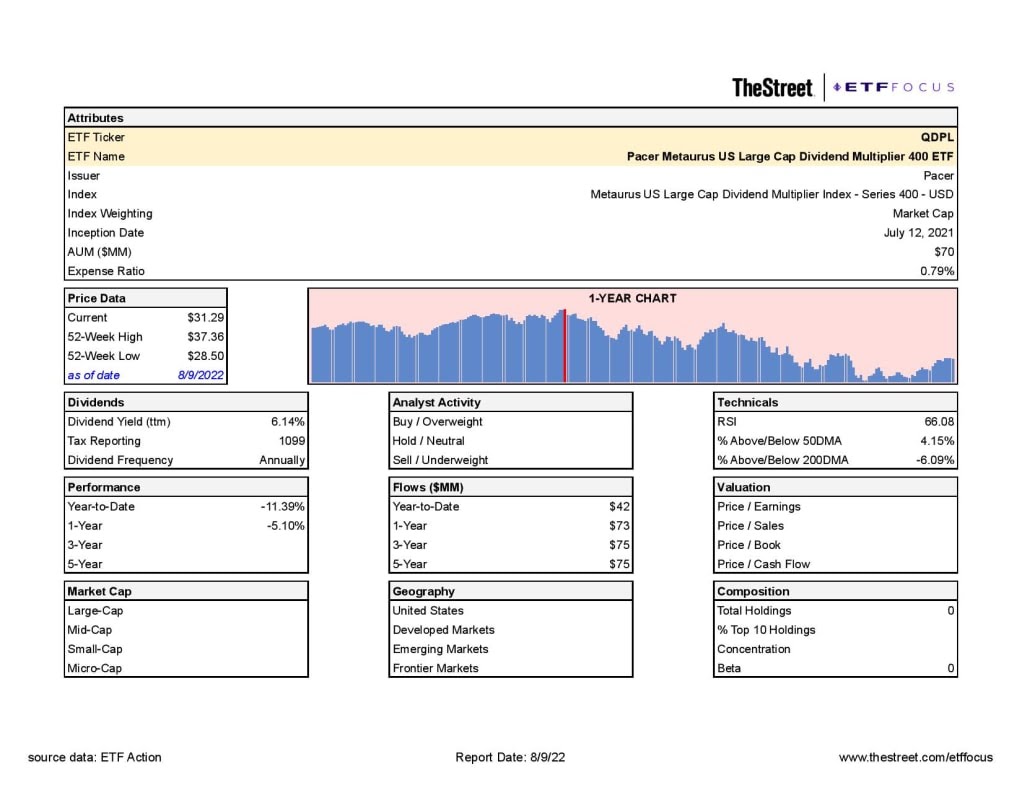

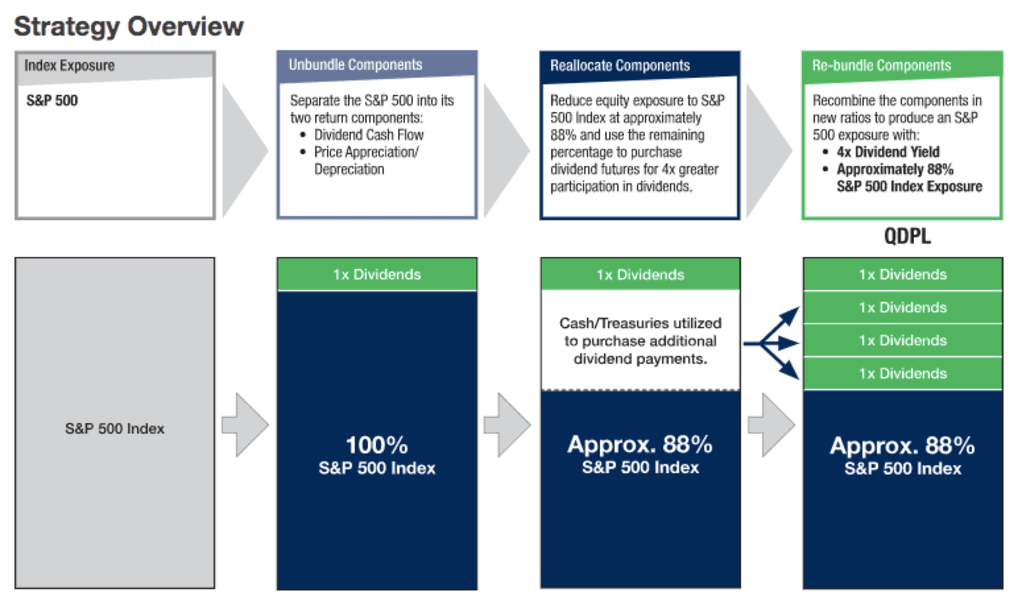

Pacer Metaurus U.S. Large Cap Dividend Multiplier 400 ETF (QDPL)

Pacer has had a blockbuster year and is one of the true up-and-comers in the ETF industry. Its foundation is the Pacer U.S. Cash Cows 100 ETF (COWZ), which focuses on major cash flow generating companies and has been a huge outperformer this year. Less known within the Pacer lineup is this ETF, which aims to quadruple the yield on the S&P 500.

QDPL kind of has the profile of a covered call ETF, but goes about it in a different. It essentially reduces its exposure to the S&P 500 and then uses those funds to amplify its dividend exposure by purchasing futures contracts. What you end up with is a portfolio whose price action is roughly 88% correlated to the underlying S&P 500 index but whose dividend yield is 4 times higher. As it stands today, that distribution yield is 7.2%.

This is actually a pretty interesting way to approach high yield generation on top of an all-equity portfolio. In a traditional covered call strategy, you can typically give up 50% to even nearly 100% of share price upside depending on how much options coverage you want to layer on and how high of a yield you want to target. You can have more extreme cases, such as the Global X covered call ETFs, where they offer 12% yields, but write options on the entire fund. QDPL offers a more modest 7%, but still gives you 88% of the share price upside. Over the long-term, that strategy probably has a higher chance of paying off.

If you’re looking for something in between QDPL and the S&P 500, there’s the Pacer Metaurus U.S. Large Cap Dividend Multiplier 300 ETF (TRPL). It offers triple the yield on the S&P 500, around 5.4% currently, but 92% of S&P 500 index exposure.

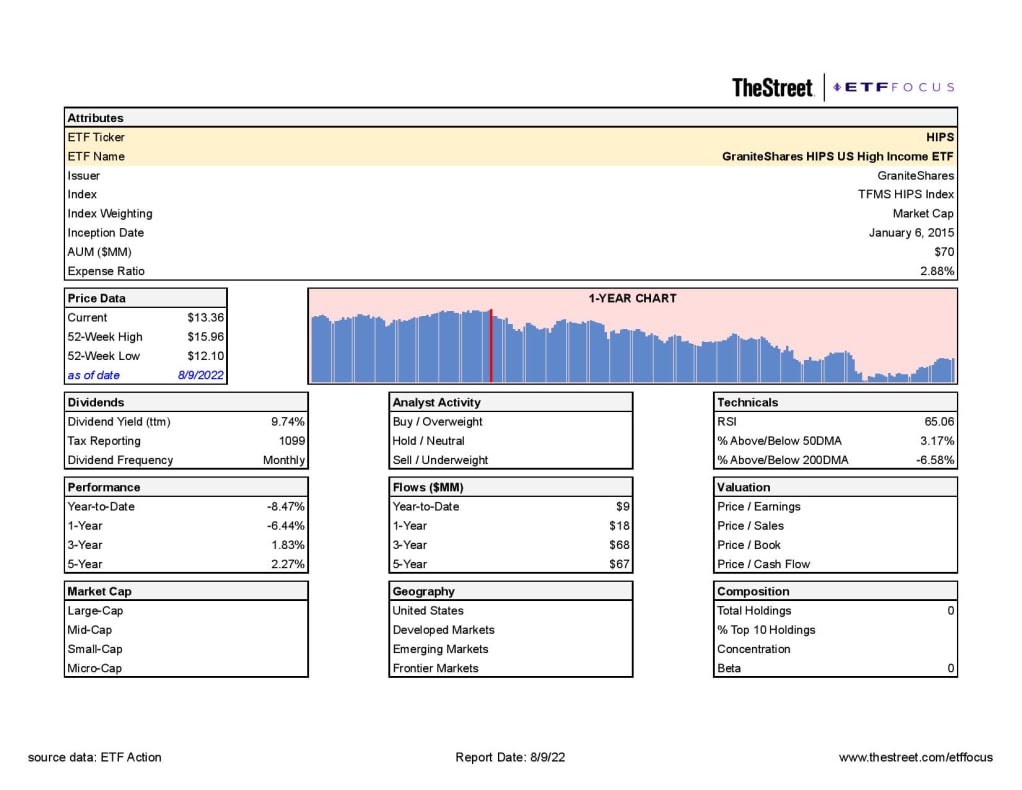

GraniteShares HIPS U.S. High Income ETF (HIPS)

HIPS is much different than any of the other four ETFs mentioned so far. It doesn’t use an options or futures based strategy. It simply invests in areas of the market that are typically known for their above average yields. The fund’s holdings typically come from one of four segments – REITs, BDCs, MLPs and closed-end funds. The latter group is the largest, accounting for about half of the fund’s assets.

Because it invests in these alternative asset classes, it does perhaps the best job of diversifying away portfolio risk. Over the past five years, this ETF has spent more time being negatively correlated to the S&P 500 than positively. That means this fund could go down when stocks are rising and vice versa, but the overall effect on the portfolio is lower risk and lower volatility. Add in a current yield that’s around 8.5% and that can be a great addition to a retirement portfolio.

On its own, HIPS is about 30-50% more volatile on a daily than the S&P 500, depending on the time frame. It can be a bit more of a wild ride in isolation, but when paired with a traditional stock/bond portfolio in moderation, it can be a great way to get a yield while potentially reducing overall portfolio risk.