The Top 7 Dividend Aristocrats Now

Analysis on our top 7 Dividend Aristocrats is below. These rankings are based on 5 year forward expected total return estimates from the Sure Analysis Research Database.

Looking to go beyond the Dividend Aristocrats?

There are ~140 securities with 25+ years of rising dividends, more than double the number of Dividend Aristocrats. That’s because the Dividend Aristocrats list excludes securities that aren’t in the S&P 500 and/or that don’t meet certain size and liquidity requirements.

Each month we rank stocks with 25+ years of rising dividends based on a mix of expected total returns and Dividend Risk Scores in our Top 10 Dividend Elite Service.

A special report of our top 10 is published on the 1st Sunday of each month.

Click here to start your free trial of this service and get your special report on our top 10 dividend stock picks with 25+ years of rising dividends.

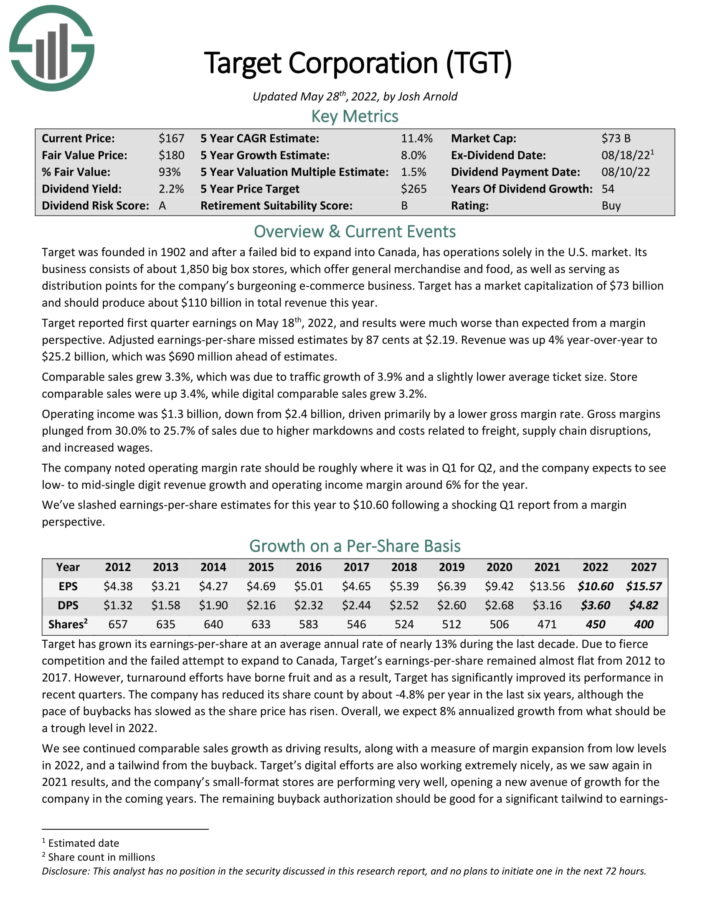

Dividend Aristocrat #7: Target Corporation (TGT)

- 5-year Expected Annual Returns: 12.1%

Target was founded in 1902 and after a failed bid to expand into Canada, has operations solely in the U.S. market. Its business consists of about 1,850 big box stores, which offer general merchandise and food, as well as serving as distribution points for the company’s burgeoning e-commerce business.

Target reported first-quarter results on May 18th. Quarterly revenue of $25.17 billion beat analyst estimates by $688 million, but earnings-per-share of $2.19 missed estimates by $0.87. Cost inflation led to the disappointing EPS figure.

We see continued comparable sales growth as driving results, along with a small measure of margin expansion, and a tailwind from the buyback. Target’s digital efforts are also working extremely nicely, and the company’s small-format stores are performing very well, opening a new avenue of growth for the company in the coming years. The remaining buyback authorization should be good for a significant tailwind to earnings-per-share in the coming years.

We expect 8% annual EPS growth through 2027. In addition, the stock has a current dividend yield of 2.3%. Lastly, the stock has a 2022 P/E of 14.9, below our fair value P/E of 17. Total returns are estimated at 12.1% per year over the next five years.

Click here to download our most recent Sure Analysis report on Target (preview of page 1 of 3 shown below):

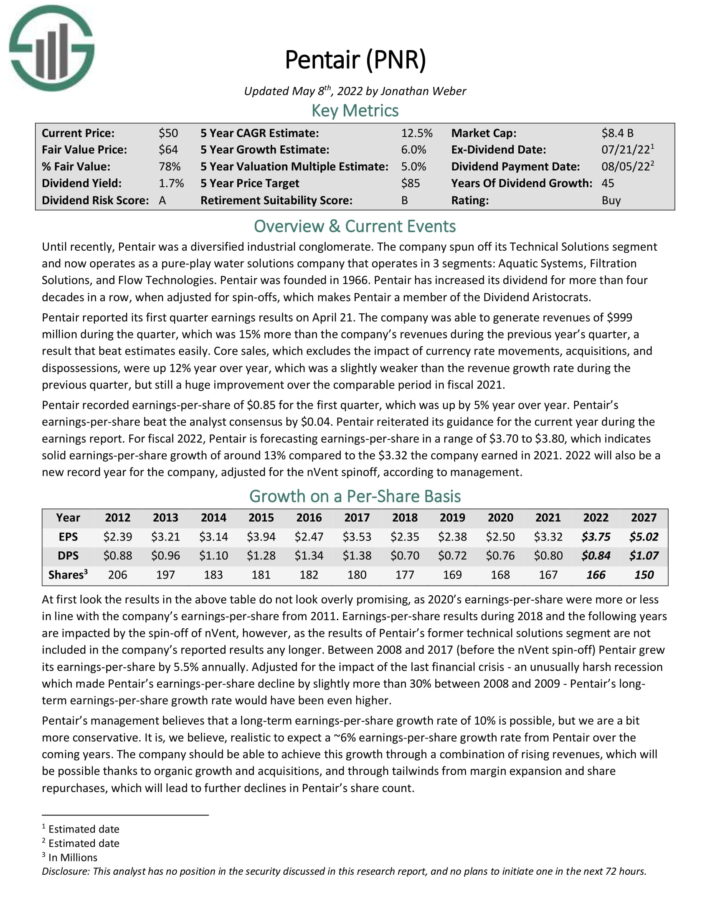

Dividend Aristocrat #6: Pentair (PNR)

- 5-year Expected Annual Returns: 12.5%

Pentair operates as a pure–play water solutions company with 3 segments: Aquatic Systems, Filtration Solutions, and Flow Technologies. Pentair was founded in 1966. Pentair has increased its dividend for more than fourdecades in a row, when adjusted for spin–offs.

Pentair reported its first-quarter earnings results on April 21. Revenues of $999 million rose 15% year-over-year, and beat estimates easily. Core sales, which excludes the impact of currency rate movements, acquisitions, and dispossessions, were up 12% year over year.

Source: Investor Presentation

Pentair recorded earnings-per-share of $0.85 for the first quarter, which was up by 5% year over year. Pentair’s earnings-per-share beat the analyst consensus by $0.04.

Pentair reiterated its guidance for the current year during the earnings report. For fiscal 2022, Pentair is forecasting earnings-per-share in a range of $3.70 to $3.80, which indicates solid earnings-per-share growth of around 13% compared to the $3.32 the company earned in 2021. 2022 will also be a new record year for the company, adjusted for the nVent spinoff, according to management.

Total returns are expected to reach 12.5% over the next five years.

Click here to download our most recent Sure Analysis report on Pentair (preview of page 1 of 3 shown below):

Dividend Aristocrat #5: Walgreens Boots Alliance (WBA)

- 5-year Expected Annual Returns: 12.6%

Walgreens Boots Alliance is the largest retail pharmacy in both the United States and Europe. Through its flagship Walgreens business and other business ventures, the company employs more than 325,000 people and has more than 13,000 stores.

On March 31st, 2022, Walgreens reported Q2 results for the period ending February 28th, 2021. Sales from continuing operations grew 3% over the prior year’s quarter, driven by COVID-19 vaccinations and testing. U.S. retail comparable sales grew 15%, which is a 20-year high growth rate.

Adjusted earnings-per-share grew 26%, from $1.26 to $1.59, and exceeded analysts’ consensus by $0.19. The company has beaten analysts’ estimates for 7 consecutive quarters.

Walgreens reiterated its guidance for low-single digit growth of its annual earnings-per-share.

We expect 5% annual EPS growth over the next five years. In addition, the stock has a 4.4% dividend yield. We also view the stock as undervalued, leading to total expected returns of 12.6% per year.

Click here to download our most recent Sure Analysis report on Walgreens (preview of page 1 of 3 shown below):

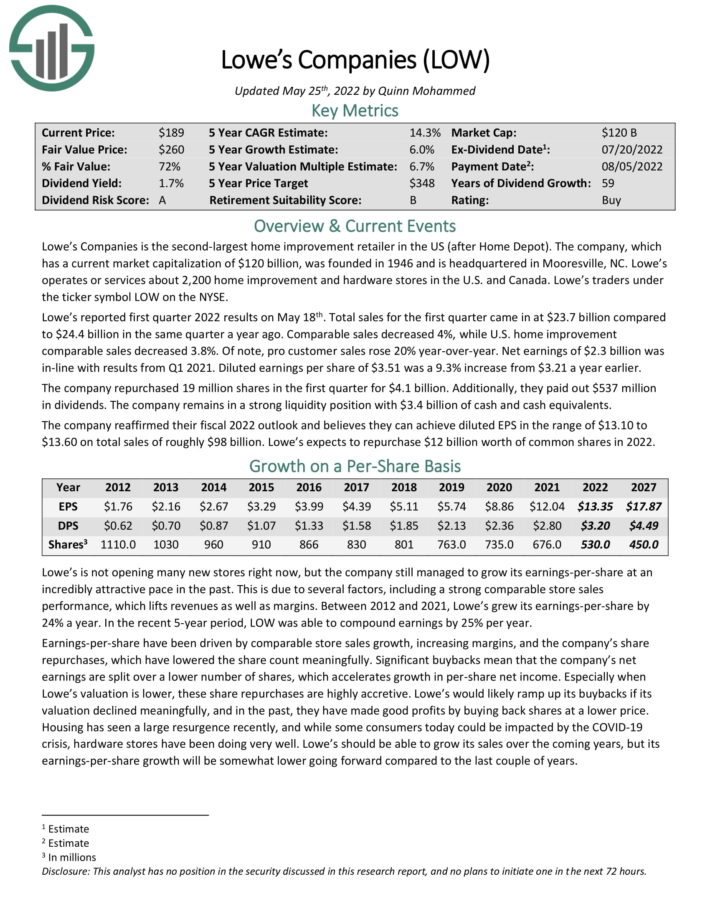

Dividend Aristocrat #4: Lowe’s Companies (LOW)

- 5-year Expected Annual Returns: 13.6%

Lowe’s Companies is the second-largest home improvement retailer in the US (after Home Depot). Lowe’s operates or services more than 2,200 home improvement and hardware stores in the U.S. and Canada.

Lowe’s reported first quarter 2022 results on May 18th. Total sales for the first quarter came in at $23.7 billion compared to $24.4 billion in the same quarter a year ago. Comparable sales decreased 4%, while U.S. home improvement comparable sales decreased 3.8%.

Of note, pro customer sales rose 20% year-over-year. Net earnings of $2.3 billion was in-line with results from Q1 2021. Diluted earnings per share of $3.51 was a 9.3% increase from $3.21 a year earlier.

The company repurchased 19 million shares in the first quarter for $4.1 billion. Additionally, they paid out $537 million in dividends. The company remains in a strong liquidity position with $3.4 billion of cash and cash equivalents.

The company provided a fiscal 2022 outlook and believes they can achieve diluted EPS in the range of $13.10 to $13.60 on total sales of roughly $98 billion. Lowe’s expects to repurchase $12 billion worth of common shares in 2022.

The combination of multiple expansion, 6% expected EPS growth and the 2.1% dividend yield lead to total expected returns of 13.6% per year.

Click here to download our most recent Sure Analysis report on Lowe’s (preview of page 1 of 3 shown below):

Dividend Aristocrat #3: V.F. Corporation (VFC)

- 5-year Expected Annual Returns: 13.9%

V.F. Corporation is one of the world’s largest apparel, footwear and accessories companies. The company’s brands include The North Face, Vans, Timberland and Dickies. The company, which has been in existence since 1899, generated over $11 billion in sales in the last 12 months.

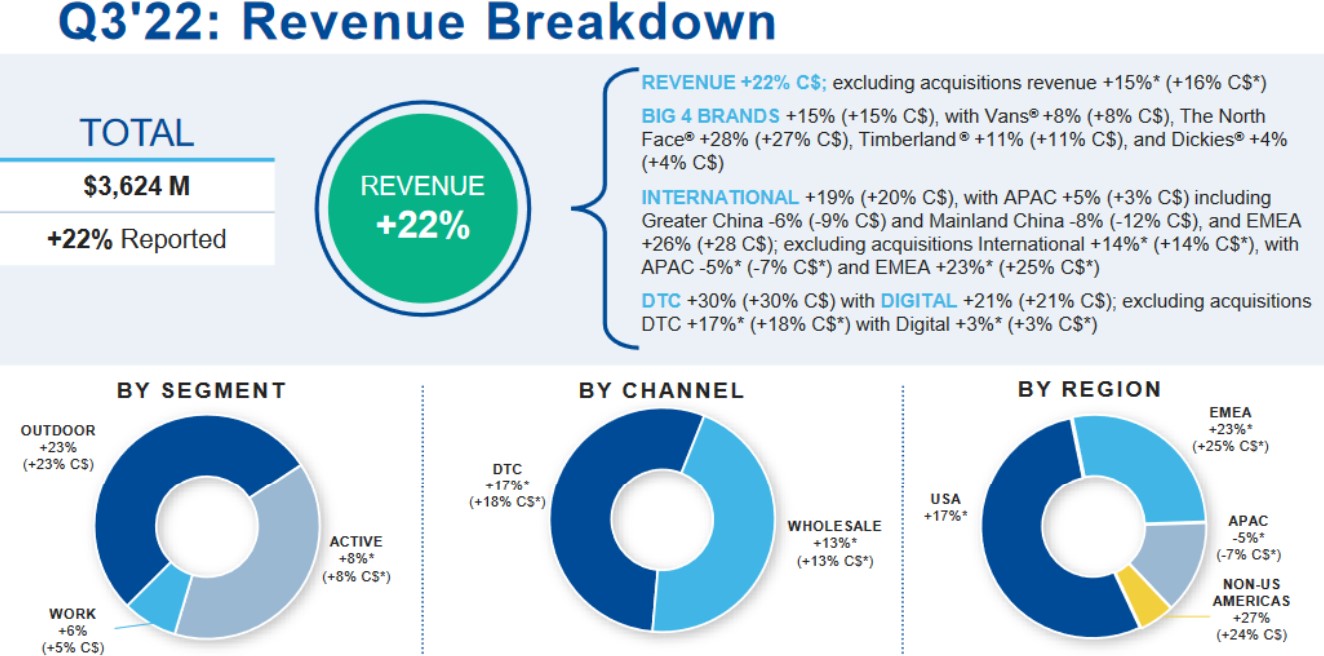

In late January, V.F. Corp reported (1/28/22) financial results for the third quarter of fiscal 2022. Revenue and organic revenue grew 22% and 15%, respectively, over the prior year’s quarter, driven by the EMEA and North American regions, which experienced a negative impact from the pandemic in the prior year’s period.

Source: Investor Presentation

Adjusted EPS grew 45%, from $0.93 to $1.35, and beat analysts’ consensus by $0.13.

For this fiscal year, V.F. Corp expects revenue of about $11.85 billion, slightly lower than the previous guidance of at least $12.0 billion but still reflecting 28% growth, and adjusted EPS to be around $3.20.

We expect 7% annual EPS growth, while the stock has a dividend yield of 4.0%. Along with a positive impact from an expanding P/E multiple, total returns are expected to reach 13.9% per year.

Click here to download our most recent Sure Analysis report on V.F. Corp. (preview of page 1 of 3 shown below):

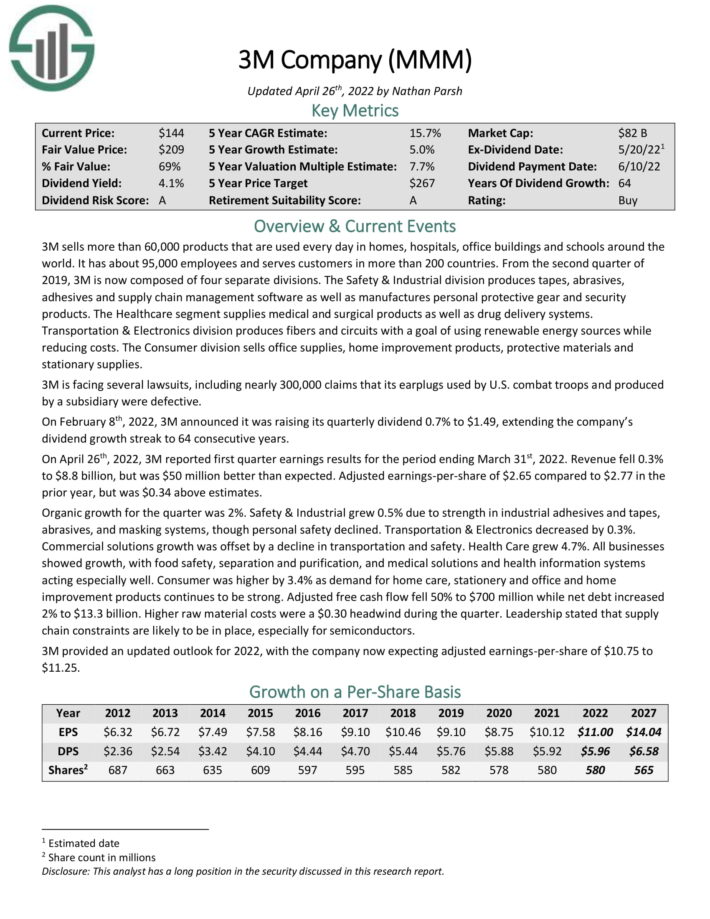

Dividend Aristocrat #2: 3M Company (MMM)

- 5-year Expected Annual Returns: 14.9%

3M sells more than 60,000 products that are used every day in homes, hospitals, office buildings and schools around the world. It has about 95,000employees and serves customers in more than 200 countries.

3M is now composed of four separate divisions. The Safety & Industrial division produces tapes, abrasives, adhesives and supply chain management software as well as manufactures personal protective gear and security products.

The Healthcare segment supplies medical and surgical products as well as drug delivery systems. Transportation & Electronics division produces fibers and circuits with a goal of using renewable energy sources while reducing costs. The Consumer division sells office supplies, home improvement products, protective materials and stationary supplies.

On April 26th, 2022, 3M reported first quarter earnings results for the period ending March 31st, 2022. Revenue fell 0.3% to $8.8 billion, but was $50 million better than expected. Adjusted earnings-per-share of $2.65 compared to $2.77 in the prior year, but was $0.34 above estimates. Organic growth for the quarter was 2%.

Source: Investor Presentation

Safety & Industrial grew 0.5% due to strength in industrial adhesives and tapes, abrasives, and masking systems, though personal safety declined. Transportation & Electronics decreased by 0.3%. Commercial solutions growth was offset by a decline in transportation and safety. Health Care grew 4.7%. Consumer was higher by 3.4% as demand for home care, stationery and office and home improvement products continues to be strong.

3M provided an updated outlook for 2022, with the company now expecting adjusted earnings-per-share of $10.75 to $11.25. Total returns are expected to reach 14.9% per year over the next five years.

Click here to download our most recent Sure Analysis report on 3M(preview of page 1 of 3 shown below):

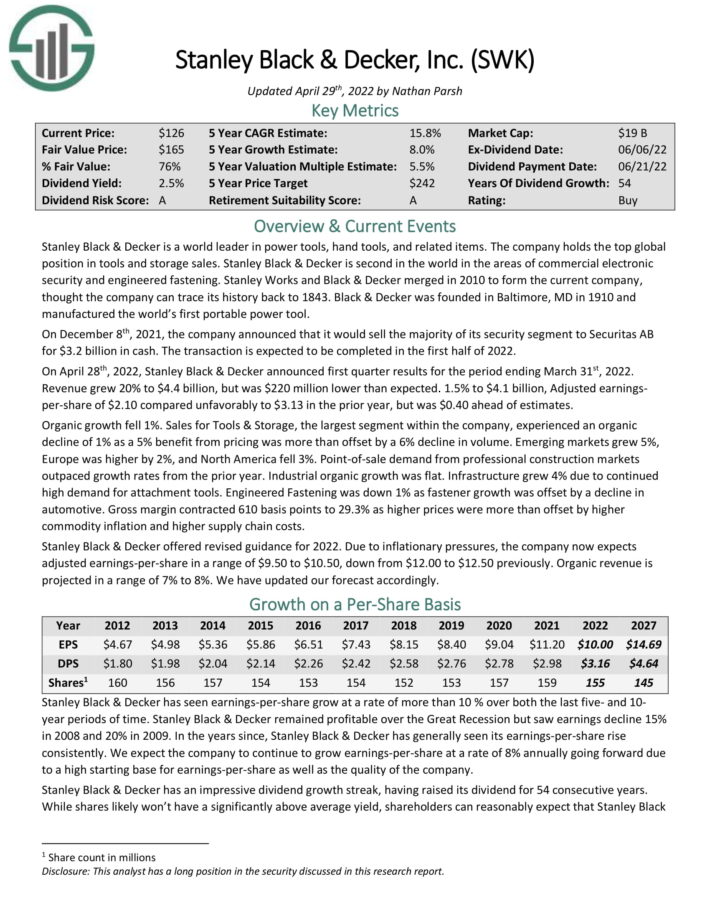

Dividend Aristocrat #1: Stanley Black & Decker (SWK)

- 5-year Expected Annual Returns: 17.2%

Stanley Black & Decker is a world leader in power tools, hand tools, and related items. The company holds the top global position in tools and storage sales. Stanley Black & Decker is second in the world in the areas of commercial electronic security and engineered fastening.

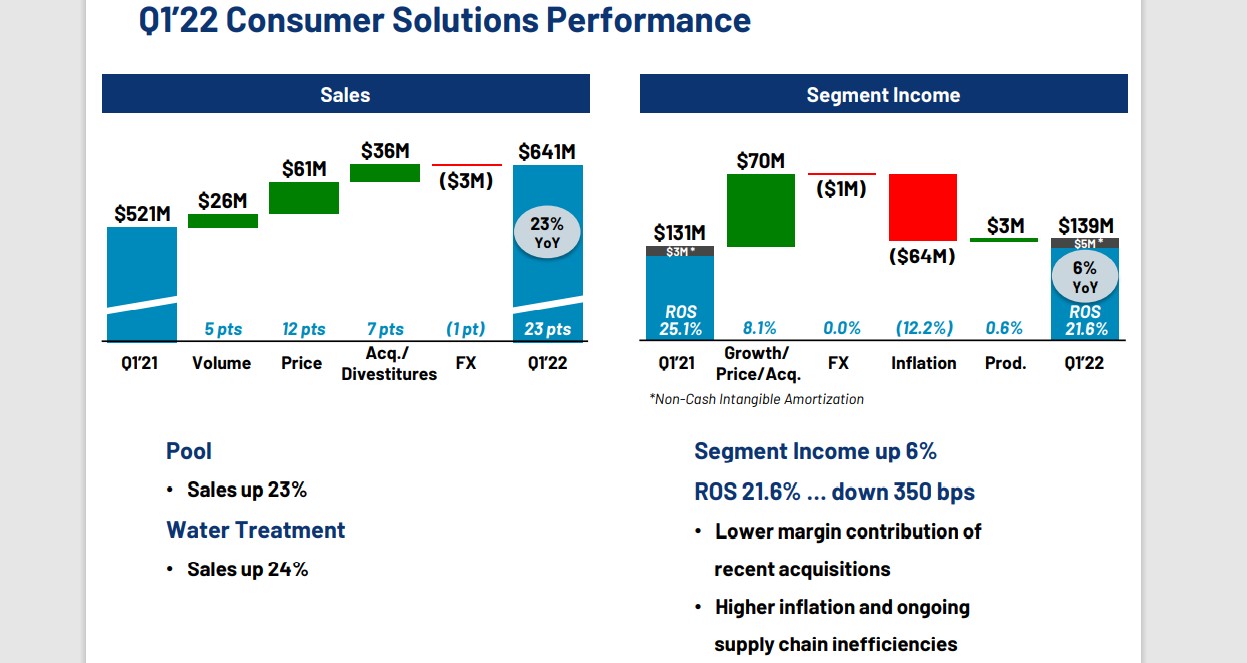

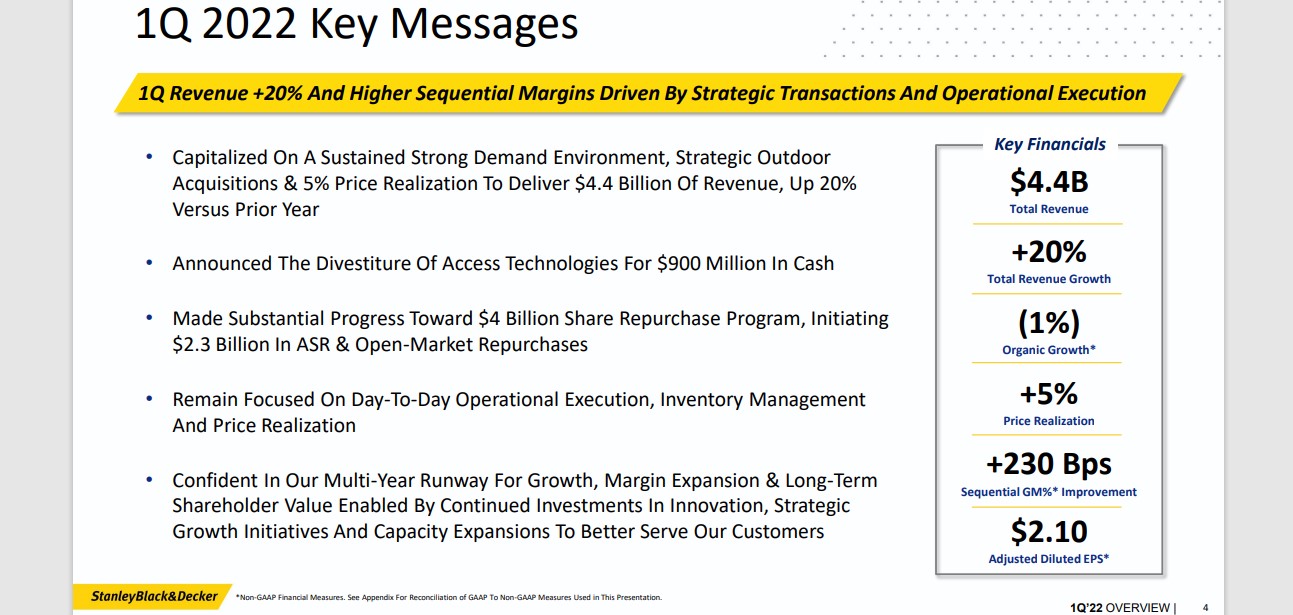

You can see an overview of the company’s 2022 first-quarter performance in the image below:

Source: Investor Presentation

On April 28th, 2022, Stanley Black & Decker announced first quarter results. Revenue grew 20% to $4.4 billion, but was $220 million lower than expected. Adjusted earnings-per-share of $2.10 compared unfavorably to $3.13 in the prior year, but was $0.40 ahead of estimates. Organic growth fell 1%.

Stanley Black & Decker offered revised guidance for 2022. Due to inflationary pressures, the company now expects adjusted earnings-per-share in a range of $9.50 to $10.50, down from $12.00 to $12.50 previously. Organic revenue is projected in a range of 7% to 8%.

The stock has a 2.7% dividend yield, and we expect 8% annual EPS growth. With a ~6.5% annual boost from an expanding P/E multiple, total returns are expected to reach 17.2% per year.

Click here to download our most recent Sure Analysis report on SWK (preview of page 1 of 3 shown below):